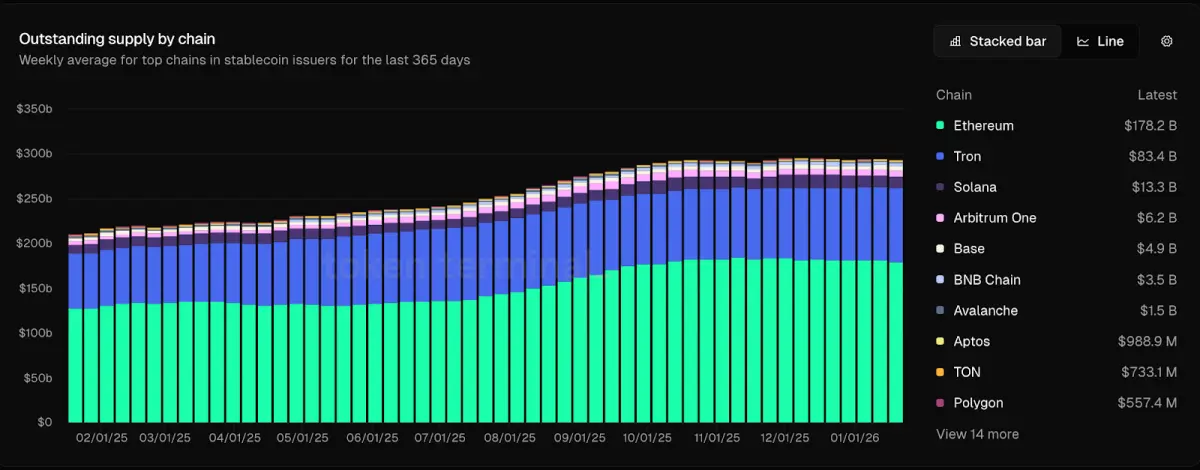

Ethereum remains the clear market leader for stablecoin issuance and settlement.

As of January 23, the ethereum mainnet hosted about 62.2% of the stablecoin market, roughly $178.20 billion out of roughly $300 billion in total supply, according to data resource Token Terminal.

Tether’s USDT remains the largest stablecoin issuer by outstanding supply, with roughly $189.2 billion in circulation at the latest reading. That is well ahead of Circle’s USDC supply of $74.6 billion.

Why Stablecoin Projects Prefer Ethereum

Most stablecoin projects launch on Ethereum for structural reasons: distribution, interoperability, and liquidity.

First, Ethereum’s token standards—especially ERC-20—give issuers a plug-and-play format supported across most wallets, exchanges, and DeFi apps. So, stablecoins can integrate quickly without custom builds.

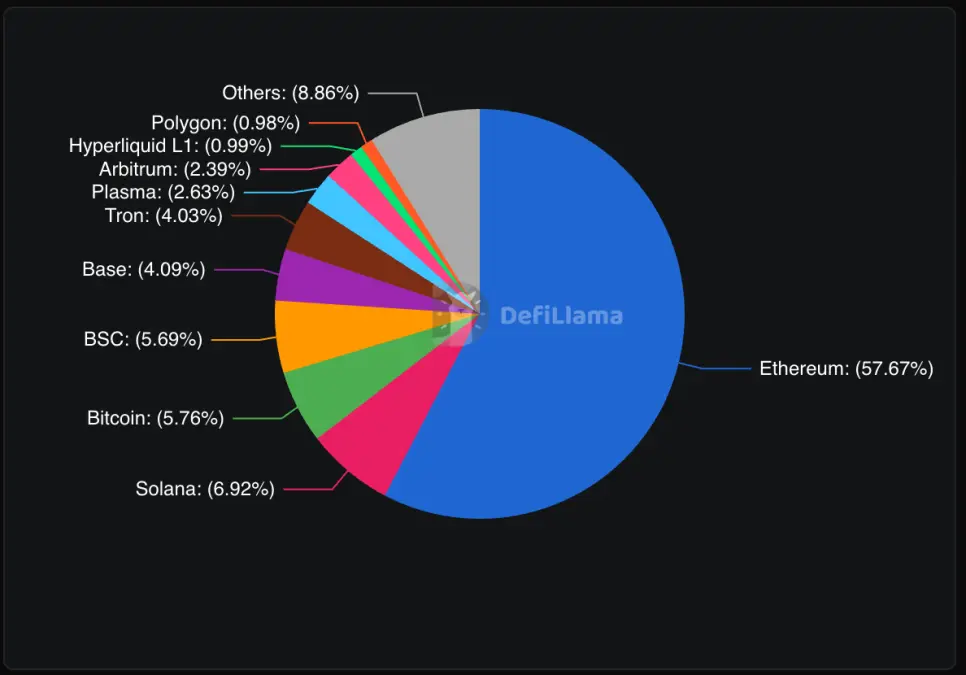

Second, Ethereum remains the largest DeFi hub by total value locked (TVL) at $69.16 billion. That makes it the easiest place to bootstrap liquidity and power core uses like trading, lending, and collateralized borrowing, where stablecoins act as the default “cash” asset.

Third, Ethereum’s rollup-centric roadmap lets stablecoins move at low cost on Layer-2 networks, while still settling back to the main chain. So, users get cheaper transfers without leaving the same standards and app ecosystem.

As a result, Ethereum also supports the broadest Layer-2 landscape, with tens of billions of dollars in TVL across its scaling networks by late 2025.

Ethereum’s stablecoin lead is also supported by ecosystem growth.

Contract deployments surged in December 2025 around the Fusaka upgrade. Fusaka targeted more data capacity and better Layer-2 economics. That can reduce congestion and lower deployment costs.

Token Terminal ranks Ethereum fourth in all-time deployments at about 94.1 million. The same rollout also strengthened the rollup stack that stablecoins use for cheaper transfers.